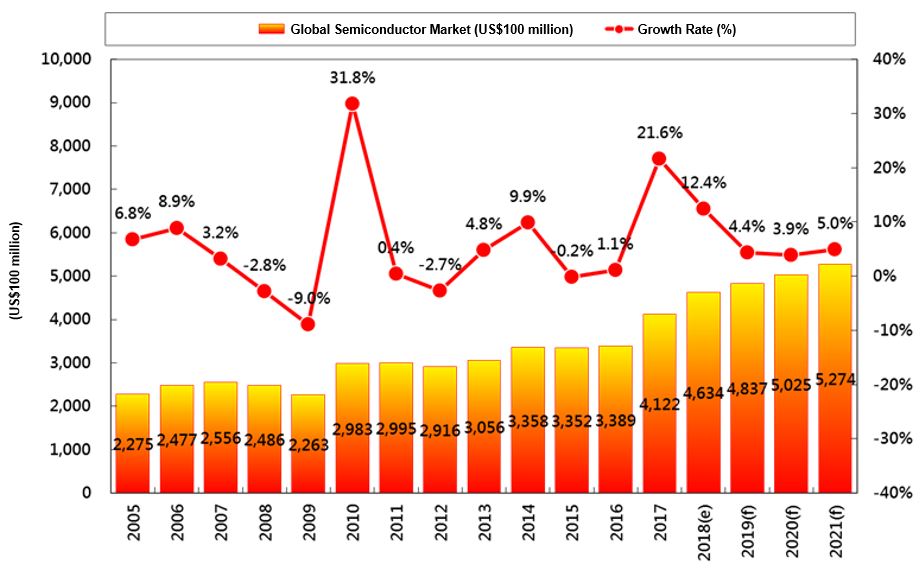

In 2017, the global semiconductor market reached USD 412.2 billion with a growth of 21.6%. It is expected to reach USD 463.4 billion in 2018 with a continuous growth of 12.4%.

Source:WSTS, ITRI-ISTI, organized by SIPO (August 2018)

Global Significance of Taiwan’s Semiconductor Industry in 2017.

The world’s No. 3 player in terms of total IC Industry output

(IC Design No.2; IC Foundry No.1; IC Packaging and Testing No.1)

|

2017 |

Output of Taiwan (US$100 Million) |

Global Output (US$100 Million) |

Taiwan’s Market Share (%) |

Taiwan’s Ranking |

Major Taiwanese Companies |

Leading Countries |

|---|---|---|---|---|---|---|

|

Output Value of IC Industry Chain =A+B+C |

810 |

5,026 |

16.1% |

No.3 |

TSMC |

The U.S. and Korea |

|

A.IC Design |

203 |

976 |

20.8% |

No.2 |

Media Tek |

The U.S. |

|

B.IDM(include Memory) |

53 |

3,277 |

1.6% |

No.5 |

Nanva Technology |

The U.S., Korea, Japan and Europe |

|

C.IC Foundry |

397 |

547 |

72.5% |

No.1 |

TSMC |

Taiwan |

|

D.IC Packaging and Testing |

157 |

281 |

55.9% |

No.1 |

ASE |

Taiwan |

|

Output Value of IC products ( IC Brand)=A+B |

256 |

4,203 |

6.1% |

No.4 |

Media Tek |

The U.S., Korea, and Japan |

-

Taiwan’s IC industry has a complete industry chain. From the upstream IC Design to the downstream IDM and IC Packaging and Testing, Taiwan has a unrivaled and professional division-of-labor structure. The output value of Taiwan’s IC industry is in the world’s third place, right after the United States and Korea (before Japan, Europe, mainland China and Singapore).

-

The world’s No. 2 player in terms of total IC Design output, right after the U.S. (before Mainland China).

-

The world’s No. 5 player in terms of total IDM output and the world’s No. 4 player in terms of total memory production output. Taiwan mainly produces DRAM, and then NOR Flash and Mask ROM. Its world position comes only after Korea, the United States and Japan.

-

The world’s No. 1 player in terms of total IC foundry output and a global leader with advanced below 10 nm production process.

-

The world’s No. 1 player in terms of IC Packaging and Testing output. Besides, among the world’s top 10 professional IC Packaging and Testing companies, more than half of them are from Taiwan.

Source:WSTS, ITRI-ISTI, organized by SIPO (August 2018)

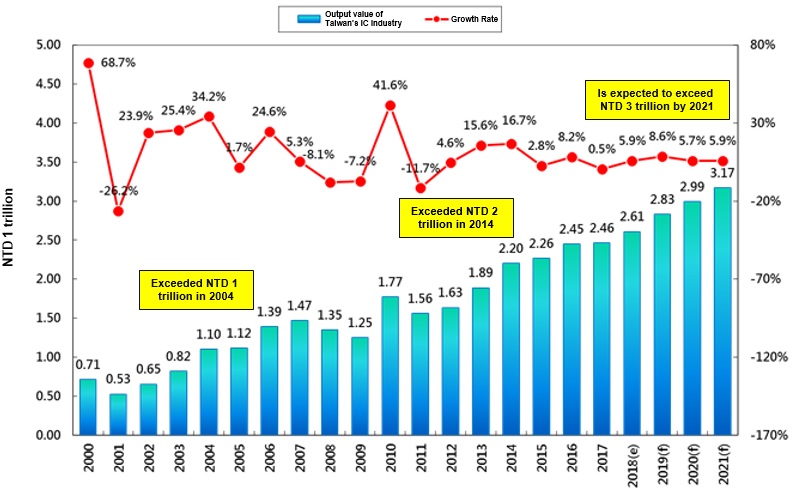

Taiwan value the development of the semiconductor industry as it facilitates the country’s economic growth and social development.

The industry’s output value is expected to reach NTD 3 trillion by 2021.

-

The output value of Taiwan’s semiconductor industry reached 2.46 trillion in 2017 with a growth of 0.5%. It is expected to reach 2.61 trillion by 2018 with a growth of 5.9%.

-

Taiwan’s IC industry has a complete industry chain. From the upstream IC Design to the downstream IDM and IC Packaging and Testing, Taiwan has a unrivaled and professional division-of-labor structure. The output value of Taiwan’s IC industry is in the world’s third place(about 20% of the market share), right after the United States and Korea.

-

The world’s No. 2 player in terms of total IC Design output (about 20% of the market share). The world’s No. 1 player in terms of total IC foundry output (about 70% of the market share). The world’s No. 1 player in terms of IC Packaging and Testing output (about 50% of the market share). The world’s No. 1 player in terms of Memory output (about 10% of the market share).

Source:TSIA, ITRI-ISTI, organized by SIPO (August 2018)

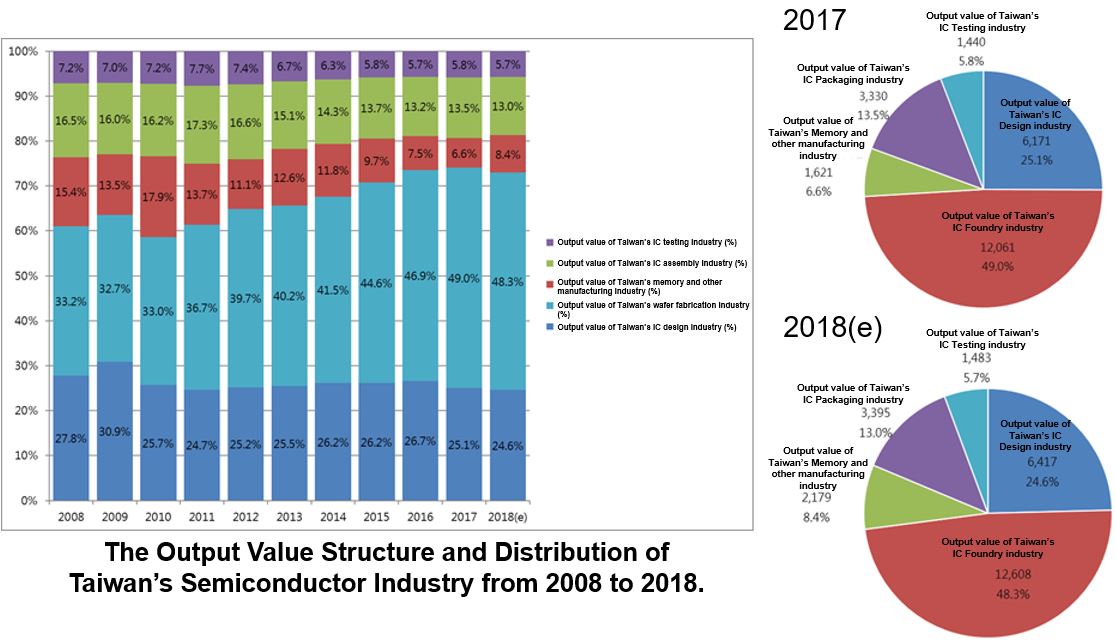

The Output Structure of Taiwan’s Semiconductor Industry.

In 2018, the proportion of IC Foundry is 48%, which has facilitated the development of IC Design (25%), IC Packaging and Testing (19%) and Memory industry (8%).

Source:TSIA, ITRI-ISTI, organized by SIPO (August 2018)